- New commitments bring total fund size close to $150m

- The fund has deployed $140m, reaching over 272k entrepreneurs in India

Mumbai, February 27, 2025: Vivriti Asset Management (VAM) has raised additional commitments of $40 million for its Vivriti India Retail Assets Fund (VIRAF) from British International Investment (BII), the UK’s development finance institution and impact investor, and Calvert Impact, a global nonprofit investment firm based in the United States, to support financial inclusion for India’s micro, small and medium enterprises (MSMEs).

India’s 63 million MSMEs contribute up to 30 percent of the country’s GDP, generate over 40 percent of exports, and create employment for over 100 million people. However, the MSME finance gap in India remains enormous at an estimated $342 billion, with MSEs accounting for 95 percent of that gap.

Launched in March 2023, at GIFT City, India’s first international financial services centre, VIRAF is a first-of-a-kind asset-backed securitization (ABS) fund in India. VIRAF seeks to scale investments in small ticket loans to MSEs, as well as individuals with a focus on women entrepreneurs.

BII committed $30 million alongside $10 million from Calvert Impact to the senior debt tranche of the fund. They joined existing investors including M&G Catalyst and IFC to bring the total fund size close to $150 million.

As of December 2024, VIRAF has cumulatively invested $140 million in 40+ ABS and bond transactions. These loans have reached over 194,000 individuals and over 78,000 MSME borrowers. Of those, approximately 76 per cent are women. Over a ten-year period, VAM aims to cumulatively invest over $1 billion in retail ABS.

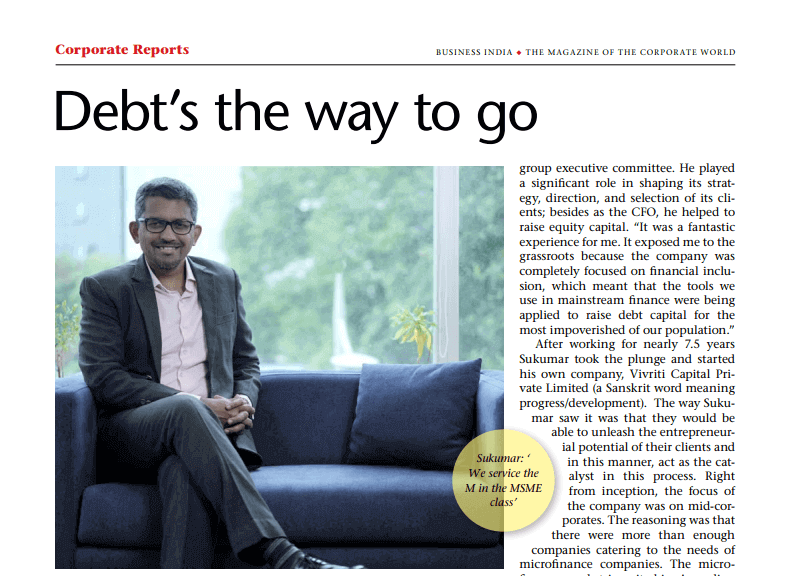

“We are pleased to partner with BII and Calvert Impact in this unique product. Their commitments serve as further validation of VIRAF’s investment thesis and success of innovative structuring which seeks to blend public capital with private capital to finance Sustainable Development Goals. The additional capital will allow us to scale VIRAF further and help demonstrate the scalability, stability and resilience of India’s ABS markets,” said Vineet Sukumar, Founder and MD, VAM.

“Supporting financial inclusion for MSMEs and women-led businesses is a key priority for us in India. To enable more accessible finance for them, we are delighted to collaborate with like-minded partners such as Vivriti Asset Management and support new financial instruments. This innovative securitisation structure will not only provide essential access to finance for local businesses but also demonstrate its commercial viability to mobilise more commercial investors,” said Srini Nagarajan, Managing Director and Head of Asia, British International Investment.

This investment supports UN SDG 5 on Gender Equality, SDG 8 on Decent Work and Economic Growth, SDG9 on Industry, Innovation and Infrastructure as well as SDG10 on Reduced Inequalities.

About VAM

Vivriti Asset Management (VAM) is a performing-credit focused asset manager, investing in debt issued by mid-sized enterprises. With commitments of c.US$625 million across 11 funds, VAM manages sector-agnostic funds that have invested across infrastructure, energy, logistics, financials, Saas and services businesses.

Vivriti Asset Management Private Limited (IFSC branch) is registered with International Financial Services Centres Authority (IFSCA) as a Registered FME (Non-Retail) and the Investment Manager for Vivriti Fixed Income Fund – Series 3 IFSC LLP (trade name of Vivriti India Retail Assets Fund). VIRAF is a restricted scheme (non-retail) under the IFSCA (Fund Management) Regulations, 2022, with a 10-year fund tenure.

About British International Investment

British International Investment is the UK’s development finance institution and impact investor. As a trusted investment partner to businesses in Africa, Asia, and the Caribbean, BII invests to create productive, sustainable, and inclusive economies in our markets. Between 2022-2026, at least 30 per cent of BII’s total new commitments by value will be in climate finance. BII is also a founding member of the 2X Challenge which has raised over $33.6 billion to empower women’s economic development. The company has investments in over 1,580 businesses across 65 countries and total net assets of £8.5 billion. For more information, visit: www.bii.co.uk | watch here. Follow British International Investment on LinkedIn and X.

For more information, visit www.vivritiamc.com

Media contacts:

VAM: Resham Chhabra, resham.chhabra@vivritiamc.com

")

")

")

")

")

")

")