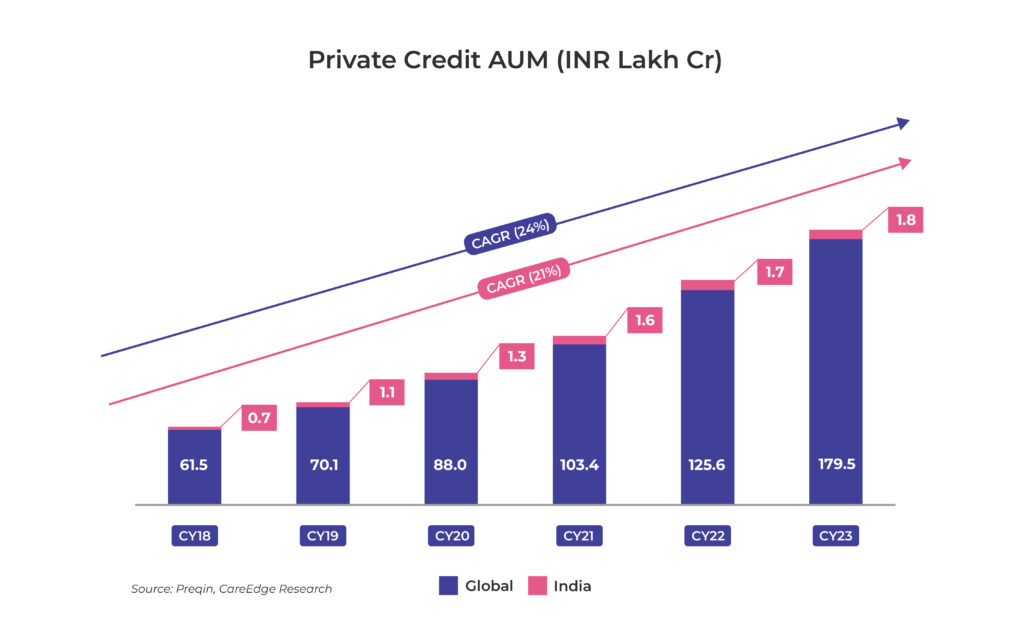

The growth in the Indian Private Credit market is driven by factors such as increasing demand for tailored debt solutions by mid-market enterprises, transformation in regulatory landscape, growing HNI population in the country (6% YoY in 2024), better risk and inflation adjusted returns compared to traditional investments, among others.

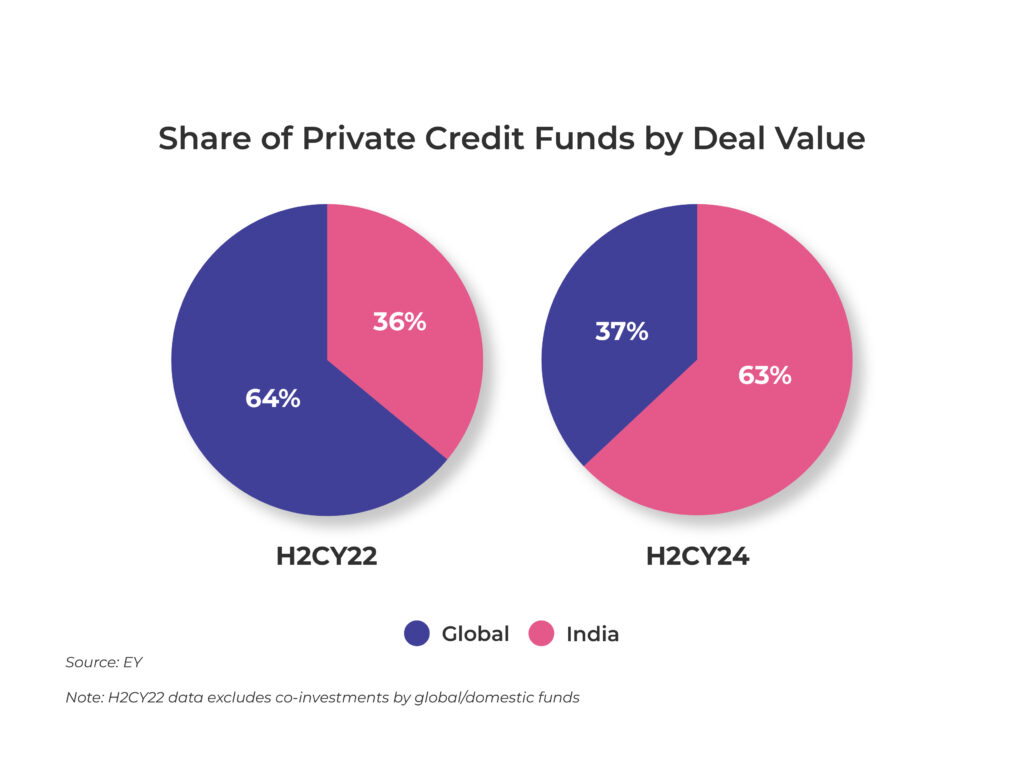

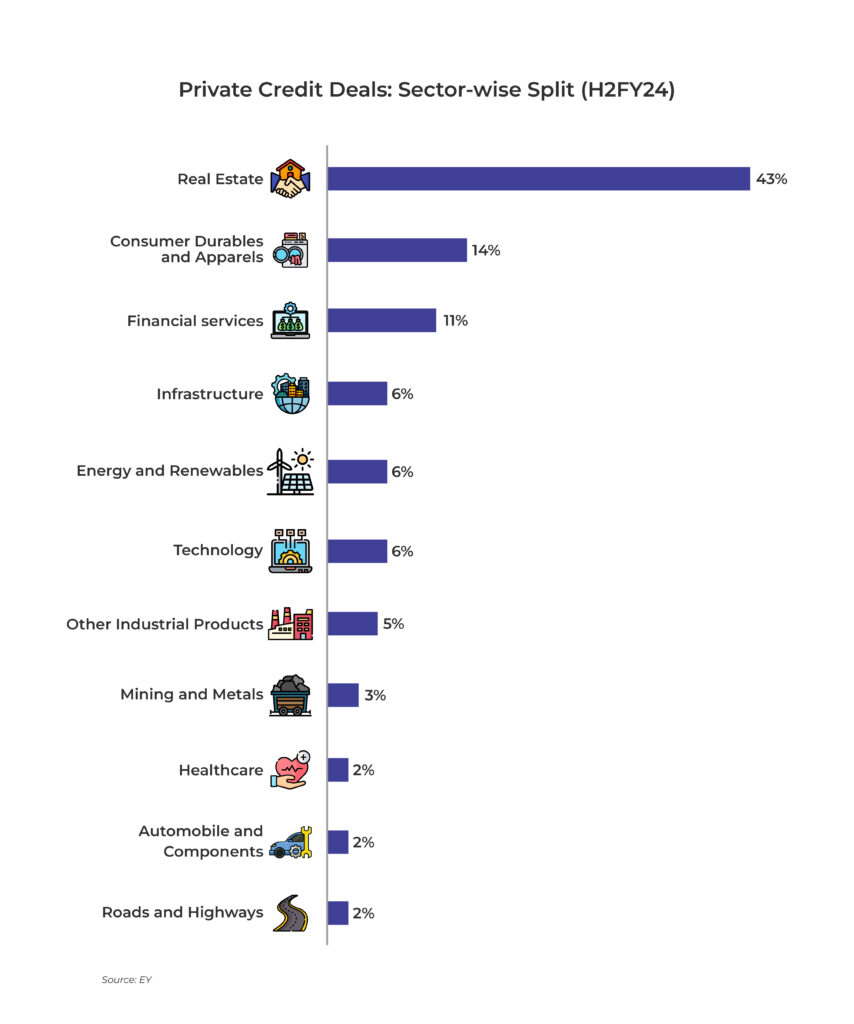

In the second half of 2024, India’s Private Credit market gained significant momentum as investments totaled ~INR 28,390 Cr which are deployed across 67 deals. Like before, real estate dominated the space, in terms of value, followed by consumer durables and apparels, and other sectors. Overall, in CY24, investments totaling ~INR 79,147 Cr were deployed across 163 deals, reflecting a YoY growth of ~7% compared.

Several Private Credit exits in H1CY24 and H2CY24 depicted a vibrant market with significant returns and evolving strategies. Going forward, confidence in the asset class is expected to grow with more and more high-net-worth individuals (HNIs) and family offices backing domestic funds and with a faster pace of growth in the economy.

Disclaimer: The information provided in this article is for general informational purposes only and is not an investment, financial, legal or tax advice. While every effort has been made to ensure the accuracy and reliability of the content, the author or publisher does not guarantee the completeness, accuracy, or timeliness of the information. Readers are advised to verify any information before making decisions based on it. The opinions expressed are solely those of the author and do not necessarily reflect the views or opinions of any organization or entity mentioned.